Written by Clyde Catton of BDO Canada LLP

The federal government introduced a major talent initiative in its 2019 budget to close skills gaps in the labour market. Called the Canada Training Benefit (CTB), the program is designed to help Canadian workers and the businesses that employ them stay current with technological change.

Canada’s labour market has shifted as business leaders automate and digitally transform their businesses. Certain jobs are becoming obsolete while new employment opportunities arise. For owner-managers, the challenge often involves finding talent skilled in the latest technologies. There may also be pressure to upgrade the skills of current employees to meet the changing needs of the business.

The CTB comprises two key components:

· A new refundable Canada Training Credit (CTC) to help eligible individuals with the cost of training fees

· Income support during training to be administered through the Employment Insurance (EI) program to assist eligible individuals during time away from work

In support of these components, the federal government also indicated that it will consult with the provinces on changes to labour laws to support new leave provisions to ensure job security for workers.

Draft legislation to implement the CTC has been tabled but not passed, and legislative changes have not been introduced for the EI benefit.

What is the Canada Training Credit?

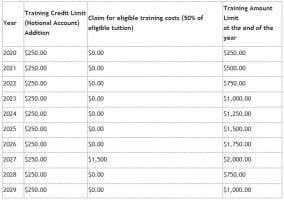

The CTC is a new refundable tax credit that will cover up to half of eligible tuition and fees associated with training, to a lifetime maximum CTC of $5,000. This represents a lifetime maximum of $10,000 in eligible tuition fees. Starting in 2020, eligible individuals will receive a credit of $250 each year towards their training amount limit in a notional account. The credit can be claimed in the year that eligible tuition fees are paid.

Example of the CTC

The following illustration shows how the CTC plan will work.

Emily is 30 years old in 2020 and is a Canadian resident. She has annual income of $70,000 in each of years 2019 to 2028. In 2027, she takes a night course at a community college to upgrade her skills. She pays the full tuition fee of $3,000 for the course.

When Emily files her 2027 tax return, she will claim a refundable tax credit of $1,500 for the CTC, reflecting the maximum claim of half of eligible tuition fees allowed. This will reduce her training amount limit in the following year. The remaining $1,500 of tuition fees not claimed for the CTC will qualify for the tuition tax credit.

Who qualifies for the CTC?

To qualify for the notional credit, each year the individual needs to meet the following tests. The individual must:

- have filed a tax return for the preceding year;

- be at least 26 years of age and not older than 65 years of age (at the end of the year);

- be resident in Canada throughout the preceding year;

- have working income of $10,000 or more in the preceding year; and

- have net income for the preceding year that does not exceed the top of the third tax bracket ($147,667 in 2019).

Working income includes income from employment; taxable research grants, fellowships, scholarships, bursaries, or prizes; business carried on by the individual (other than income earned as a specified member of a partnership); maternity and parental EI benefits, and certain other amounts that are exempt from tax.

Other details of the CTC

Annual accumulation of the training amount limit will begin in 2020. This means that an eligible individual can start to claim the CTC on eligible training fees incurred in 2020 and receive money back when they file their tax return in 2021. However, as the plan is to start in 2020, it will take until 2040 to reach the maximum $5,000 refundable credit.

The cumulative training amount limit will be included in the Notice of Assessment that the Canada Revenue Agency sends to each taxpayer each year after they file their tax return. Note that any unused training amount limit will expire at the end of the year in which an individual turns 65.

What training fees are eligible for the CTC?

An individual can apply their training amount limit against up to half the cost of eligible training fees. This includes fees paid to a university, college, or other educational institution for courses at a post-secondary level or occupational skills courses certified by the Minister of Employment and Social Development. Note that CTC eligibility is generally the same as for the tuition tax credit except that fees paid to educational institutions outside Canada will not qualify. The portion of fees refunded through the CTC will not qualify for the tuition tax credit.

EI Training Support Benefit

To help workers take time away from work to upgrade their skills, a new EI Training Support Benefit will provide up to four weeks of income support for eligible workers every four years. This benefit will be paid at 55% of an individual’s average weekly insurable earnings, subject to EI limits, and is expected to be launched in late 2020.

Because this new benefit is funded through the EI program, the government also announced a new EI Small Business Premium Rebate to offset the upward pressure on EI premiums. This rebate will also start in 2020 and will be available for businesses that pay employer EI premiums of no more than $20,000 per year.

Job security during training

The federal government will also be working with the provinces on leave provisions to support workers during training. This initiative will be aimed at helping workers take time away from work to pursue training of their choice without the risk of losing their jobs.

Guidance for business owners

As a business owner, you may be happy to see the federal government address skills shortages in the Canadian labour market. You may even be thinking of taking advantage of the CTC yourself to stay current.

However, from an operations perspective, planning will be required to keep business disruption to a minimum when employees take time off for training purposes. In addition, you may want to consider how best to encourage employees to choose courses that align with your business’s needs while considering their career goals. This can contribute to an ongoing mutually beneficial relationship with your employees.

Please contact our office at 905-576-3430 if you have any questions or would like more any information on the foregoing.

This material is general in nature and should not be relied upon to replace the requirement for specific professional advice.

This article is from BDO Tax Factor 2019-06, a publication by BDO Canada © BDO 2019

Submitted by Clyde Catton, BBA, CPA, CA, Tax Partner